Intrinsic Value — The Warren Buffett Way

How does Warren Buffett calculate intrinsic value? How does he define it? When does he use it to value a business? How to calculate owner earnings? This post will answer every question.

Warren Buffett retired a few days ago after being CEO of Berkshire Hathaway for over 60 years. He has taught countless investors how to approach investing in securities the right way, not viewing them as moving charts and a ticker symbol, but as buying a part of a business. When valuing a business, Ben Graham taught him to calculate the intrinsic value of each company before investing in them, and apply a “Margin of Safety”. Some people may ask to themselves “how can I calculate this?”, or “what does it really measure?”. Well, this is what I will try to answer today.

Buffett has given many speeches on how he approaches intrinsic value, so with all the information available to the pubic, I extracted some of the most important things he said throughout the years in his Berkshire Hathaway annual meetings, as well as a masterclass he gave in 2001. I have condensed some speeches for simplicity, but everything he said is practically there, unchanged from the original.

July 18, 2001: The Masterclass

Warren gives a masterclass about investing, mainly by answering questions from the students studying in the University of Georgia, specifically at the Terry College of Business. One student asks 2 short questions about calculating intrinsic value:

Question number one:

How do you find intrinsic value in a company?

Well, intrinsic value is what is the number that, if you were all-knowing about the future and could predict all the cash that a business would give you between now and Judgment Day, discounted at the proper discount rate, that number is what the intrinsic value of businesses is. In other words, the only reason for making investment and laying out money now is to get more money later on. That’s what investing is all about.

Now, when you look at the bond you know what you’re gonna get back, it says it right on the bond. It says when you get the interest payments, it says when you get the principal, so it’s very easy to figure out the value of a bond. The cash flows are printed on the bond. The cash flows aren’t printed on a stock certificate. That’s the job of the analyst, is to take that stock certificate, which represents an interest in the business, and change that into a bond and say, “This is what I think it’s going to pay out in the future.”

It’s the same thing for a big business. If you buy Coca-Cola today, the company is selling for about a hundred and ten to fifteen billion dollars in the market. The question is, would you lay it out today to get what the Coca-Cola company is going to deliver to you over the next two or three hundred years?

How much cash they’re going to give you isn’t a question of how many analysts are gonna recommend it, or what the volume in the stock is, or what the chart looks like. It’s a question of how much it’s going to give you. It’s true if you’re buying a farm. It’s true if you’re buying an apartment house. You’re laying out cash now to get your cash back later on. And the question is, how much you’re gonna get, and how sure are you.

When I calculate intrinsic value of a business, whether we’re buying all of a business or a little piece of a business, I always think we’re buying the whole business. I look at it and say, what will come out of this business, and when?

Berkshire has never distributed anything to its shareholders, but its ability to distribute goes up as the value of the businesses we own increases. The real question is, if you’re gonna buy the whole company for a hundred and five billion now, can we distribute enough cash to you soon enough, at present interest rates, to lay out that cash now? If you can’t answer that question, you can’t buy the stock.

There’s a lot of companies that I can’t answer that for, and I just stay away from those.

Question number two:

So you get formulas involved in finding intrinsic values on certain companies. I mean, you’ve got a mathematical. It’s not just got a present value of future cash out. Second question is, why haven’t you written down your set of formulas or your strategies in written forms that you can share with everyone else?

I think I actually have written about that. If you read the annual reports over the years, I use the illustration of Aesop. He said, “A bird in the hand is worth two in the bush.” Now, that isn’t quite complete, because the question is, how sure are you that there are two in the bush, and how long do you have to wait to get them out?

That’s all there is to investing: how many birds are in the bush, when are you gonna get them out, and how sure are you. If interest rates are fifteen percent, you’ve got to get two birds out of the bush in five years to equal the bird in the hand. If interest rates are three percent and you can get two birds out in twenty years, it still makes sense, because it all gets back to discounting against an interest rate.

May 3, 1999: Berkshire Hathaway Annual Meeting

It’s the Berkshire Hathaway annual meeting in 1999. Dan Kur, and investor from Bonita Springs, Florida, attempts to calculate the intrinsic value of Berkshire:

Dan Kur: You’ve given many clues to investors to help them calculate Berkshire’s intrinsic value. I’ve attempted to calculate the intrinsic value of Berkshire using the discounted present value of its total look-through earnings. I’ve taken Berkshire’s total look-through earnings and adjusted them for normalized earnings at GEICO, the Supercat business, and General Re. Then I’ve assumed that Berkshire’s total look-through earnings will grow at 15% per annum on average for 10 years, 10% per annum for years 11 through 20, and that earnings stop growing after year 20, resulting in a coupon equaling year 20 earnings from the 21st year onward. Lastly, I’ve discounted those estimated earnings streams at 10% to get an estimate of Berkshire’s intrinsic value.

My question is, is this a sound method? Is there a risk-free interest rate, such as a 30-year Treasury, which might be the more appropriate rate to use here, given the predictable nature of your consolidated income stream? Thank you.

Well, that is a very good question. Investment is the process of putting out money today to get more money back at some point in the future. And the question is how far in the future, how much money, and what is the appropriate discount rate to take it back to the present day and determine how much you pay.

And I would say you’ve stated the approach. I couldn’t state it better myself. The exact figures you want to use, whether you want to use 15% gains in earnings or 10% gains in the second decade, I have no comment on those particular numbers. But you have the right approach.

We would probably use the long-term government rate to discount it back, but we wouldn’t pay that number after we discounted it back. We would look for appropriate discounts from that figure. But it doesn’t really make any difference whether you use a higher figure and then look across them, or use our figure and look for the biggest discount. You’ve got the right approach.

We try to give you all of the information that we would find useful ourselves in evaluating Berkshire’s intrinsic value in our reports. I can’t think of anything we leave out of our published materials.

Now, one important element in Berkshire is that because we retain all earnings and because we have a growth of float over time, we have a considerable amount of money to invest. And it really is the success with which we invest those retained earnings and growth in float that will be an important factor in how fast our intrinsic value grows. And to an important extent, what happens there is out of our control.

If we run into favorable external circumstances, your calculation of intrinsic value would result in a higher number than if we run into the kind of circumstances that we’ve had the last 12 months.

Charlie: For many decades around here, we’ve had more than 100% of book net worth in marketable securities and a lot of wonderful wholly owned subsidiaries. We still got the wonderful businesses, but we’re having trouble with the new money.

May 5, 1997: Berkshire Hathaway Annual Meeting

It’s another Berkshire Hathaway annual meeting, this time from 1997. Fred Kocher from Boulder, Colorado, is the first person to ask a question after Kelly tells Buffett “we should start with number two, zone two”. Here they not only talk about intrinsic value, but also opportunity cost, which are two concepts highly correlated:

Fred Kocher: This is a question about intrinsic value, and it’s a question for both of you (referring Warren Buffett and Charlie Munger), because you have written that perhaps you would come up with different answers. You write and speak a great deal about intrinsic value, and you indicate that you try to give shareholders the tools in the annual report so they can come to their own determination.

What I’d like you to do is expand upon that a little bit. First of all, what do you believe to be the important tools, either in the Berkshire annual report or other annual reports that you review, in determining intrinsic value? Secondly, what rules or principles or standards do you use in applying those tools? And lastly, how does that process relate to what you have previously described as the filters you use in determining your evaluation of a company?

Warren Buffett: If we could see, in looking at any business, what its future cash inflows or outflows from the business to the owners would be over the next hundred years, or until the business is extinct, and then discount that back at the appropriate interest rate, that would give us a number for intrinsic value. It would be like looking at a bond that had a whole bunch of coupons on it. If you could see what those coupons are, you could figure the value of that bond. Businesses have coupons that are going to develop in the future. The only problem is they aren’t printed on the instrument, and it’s up to the investor to try to estimate what those coupons are going to be over time.

In high-tech businesses, we don’t have the faintest idea what the coupons are going to be. When we get into businesses where we think we can understand them reasonably well, we are trying to print the coupons. We are trying to figure out what businesses are going to be worth in 10 or 20 years. When we bought See’s Candy in 1972, we had to come to the judgment as to whether we could figure out the competitive forces that would operate and how that would look over a long period. And if you attempt to assess intrinsic value, it all relates to cash flows. The only reason for putting cash into any kind of investment now is because you expect to take cash out by what the asset itself produces.

That’s true if you’re buying a farm. It’s true if you’re buying a business. The filters you described are designed to make sure we’re in businesses where we have a high degree of confidence that we’re in the ballpark. We basically use long-term, risk-free government bond–type interest rates to think back in terms of what we should discount at. That’s what investment is all about: putting out money to get more money back later on from the asset itself.

If you’re an investor, you’re looking at what the asset is going to do. If you’re a speculator, you’re focusing on what the price is going to do, and that’s not our game. If we’re right about the business, we’re going to make money, and if we’re wrong, we don’t expect to. In looking at Berkshire, we try to tell you as much as possible about our business. We give you the information that, if the positions were reversed, we would want to get from you. In companies like Coca-Cola or Gillette or Disney, you can understand what they’re doing and then sit down and try to print out the future.

Charlie Munger: One filter that’s useful in investing is the idea of opportunity cost. If you already have something you like better than 98% of things you see, you can screen out the rest. People who use opportunity cost tend to make better investments. That leads to a concentrated portfolio, which we don’t mind.

Warren Buffett: If somebody shows us a business, the first thing we ask is whether we would rather own that or more Coca-Cola. There are very few businesses we’re as certain about as those, and we measure everything against that standard.

Charlie Munger: The concept of intrinsic value used to be easier when you could buy stocks at huge discounts to liquidation value. No matter how bad the management, you had a lot going for you. That’s much harder to find now. Those simple systems don’t work anymore. You’ve got to get into Warren’s kind of thinking, and that is a lot harder. I think you can predict the future best where the business is simple and understandable. You don’t need complex models; you just need to really understand a few simple things.

Warren Buffett: Charlie talks about liquidation value. You don’t talk about closing up the enterprise, but about what somebody else would pay for that stream of cash. You could have looked at a collection of television stations owned by Cap Cities, for example, in 1974, and it would have been worth four times what the company was selling for. Not because you’d close the stations, but because their stream of income was worth that to somebody else. The marketplace was very distressed. On a negotiated basis, you could have sold the properties for four times what the company was selling for, and you got wonderful management.

Those things happen in markets, and they will happen again. But part of investing in calculating intrinsic value is, if you get the wrong answer, if it says don’t buy, you can’t buy just because somebody else thinks it’s gonna go up, or because your friends have made a lot of easy money lately. You have to be able to walk away from anything that doesn’t work. And very few things work these days. You also have to walk away from anything you don’t understand. You would agree with that, Charlie?

Charlie Munger: Yeah. And it’s harder now partly because of the amount of capital we run. If we were running a small amount of money, our opportunities would be much greater. Our universe of ideas would expand by a huge factor.

We are looking at things today that, by their nature, a lot of people are looking at. There were times in the past when we were looking at things that very few people were looking at. And there were other times in the past when we were looking at things where the whole world was just looking at them kind of crazy. And that’s a decided help.

February 27, 1986: Berkshire Hathaway Shareholder Letter

As Buffett mentioned in his 2001 masterclass, he has indeed written before about how he approaches calculating intrinsic value. At the end of his 1986 letter to shareholders, in section “Purchase-Price Accounting Adjustments and the Cash Flow Fallacy”, he presents a short quiz. “Which business is the more valuable?”:

(None of the following is redacted or summarized, everything is complete from that specific section and in Warren E. Buffett’s exact wording)

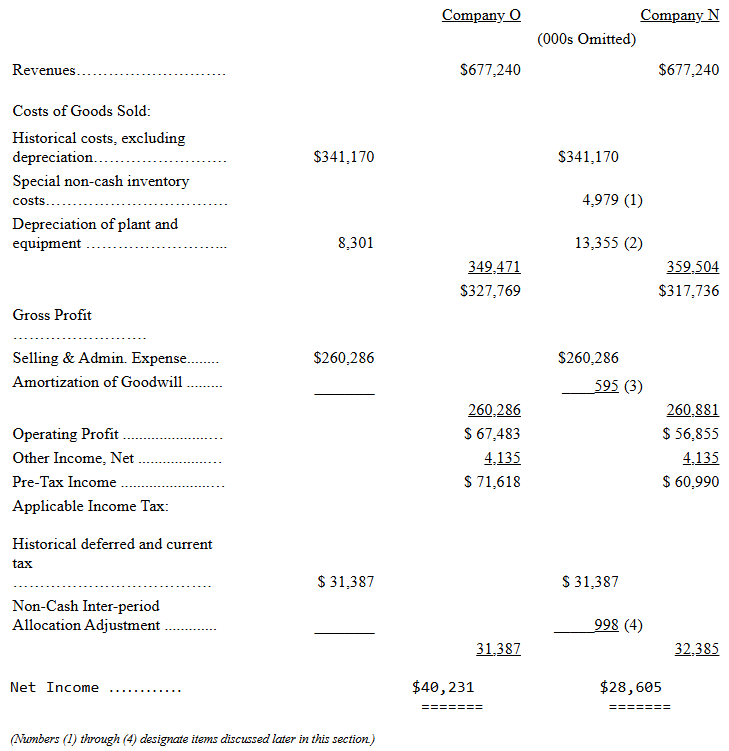

First a short quiz: below are abbreviated 1986 statements of earnings for two companies. Which business is the more valuable?

As you’ve probably guessed, Companies O and N are the same business - Scott Fetzer. In the “O” (for “old”) column we have shown what the company’s 1986 GAAP earnings would have been if we had not purchased it; in the “N” (for “new”) column we have shown Scott Fetzer’s GAAP earnings as actually reported by Berkshire.

It should be emphasized that the two columns depict identical economics - i.e., the same sales, wages, taxes, etc. And both “companies” generate the same amount of cash for owners. Only the accounting is different.

So, fellow philosophers, which column presents truth? Upon which set of numbers should managers and investors focus?

Before we tackle those questions, let’s look at what produces the disparity between O and N. We will simplify our discussion in some respects, but the simplification should not produce any inaccuracies in analysis or conclusions.

The contrast between O and N comes about because we paid an amount for Scott Fetzer that was different from its stated net worth. Under GAAP, such differences - such premiums or discounts - must be accounted for by “purchase-price adjustments.” In Scott Fetzer’s case, we paid $315 million for net assets that were carried on its books at $172.4 million. So we paid a premium of $142.6 million.

The first step in accounting for any premium paid is to adjust the carrying value of current assets to current values. In practice, this requirement usually does not affect receivables, which are routinely carried at current value, but often affects inventories. Because of a $22.9 million LIFO reserve and other accounting intricacies, Scott Fetzer’s inventory account was carried at a $37.3 million discount from current value. So, making our first accounting move, we used $37.3 million of our $142.6 million premium to increase the carrying value of the inventory.

Assuming any premium is left after current assets are adjusted, the next step is to adjust fixed assets to current value. In our case, this adjustment also required a few accounting acrobatics relating to deferred taxes. Since this has been billed as a simplified discussion, I will skip the details and give you the bottom line: $68.0 million was added to fixed assets and $13.0 million was eliminated from deferred tax liabilities. After making this $81.0 million adjustment, we were left with $24.3 million of premium to allocate.

Had our situation called for them two steps would next have been required: the adjustment of intangible assets other than Goodwill to current fair values, and the restatement of liabilities to current fair values, a requirement that typically affects only long-term debt and unfunded pension liabilities. In Scott Fetzer’s case, however, neither of these steps was necessary.

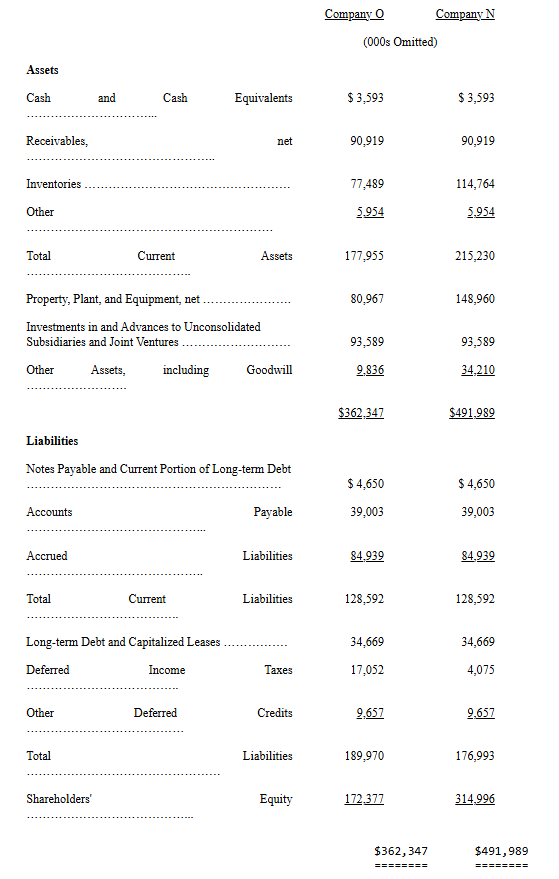

The final accounting adjustment we needed to make, after recording fair market values for all assets and liabilities, was the assignment of the residual premium to Goodwill (technically known as “excess of cost over the fair value of net assets acquired”). This residual amounted to $24.3 million. Thus, the balance sheet of Scott Fetzer immediately before the acquisition, which is summarized below in column O, was transformed by the purchase into the balance sheet shown in column N. In real terms, both balance sheets depict the same assets and liabilities - but, as you can see, certain figures differ significantly.

The higher balance sheet figures shown in column N produce the lower income figures shown in column N of the earnings statement presented earlier. This is the result of the asset write-ups and of the fact that some of the written-up assets must be depreciated or amortized. The higher the asset figure, the higher the annual depreciation or amortization charge to earnings must be. The charges that flowed to the earnings statement because of the balance sheet write-ups were numbered in the statement of earnings shown earlier:

$4,979,000 for non-cash inventory costs resulting, primarily, from reductions that Scott Fetzer made in its inventories during 1986; charges of this kind are apt to be small or non-existent in future years.

$5,054,000 for extra depreciation attributable to the write-up of fixed assets; a charge approximating this amount will probably be made annually for 12 more years.

$595,000 for amortization of Goodwill; this charge will be made annually for 39 more years in a slightly larger amount because our purchase was made on January 6 and, therefore, the 1986 figure applies to only 98% of the year.

$998,000 for deferred-tax acrobatics that are beyond my ability to explain briefly (or perhaps even non-briefly); a charge approximating this amount will probably be made annually for 12 more years.

It is important to understand that none of these newly-created accounting costs, totaling $11.6 million, are deductible for income tax purposes. The “new” Scott Fetzer pays exactly the same tax as the “old” Scott Fetzer would have, even though the GAAP earnings of the two entities differ greatly. And, in respect to operating earnings, that would be true in the future also. However, in the unlikely event that Scott Fetzer sells one of its businesses, the tax consequences to the “old” and “new” company might differ widely.

By the end of 1986 the difference between the net worth of the “old” and “new” Scott Fetzer had been reduced from $142.6 million to $131.0 million by means of the extra $11.6 million that was charged to earnings of the new entity. As the years go by, similar charges to earnings will cause most of the premium to disappear, and the two balance sheets will converge. However, the higher land values and most of the higher inventory values that were established on the new balance sheet will remain unless land is disposed of or inventory levels are further reduced.

What does all this mean for owners? Did the shareholders of Berkshire buy a business that earned $40.2 million in 1986 or did they buy one earning $28.6 million? Were those $11.6 million of new charges a real economic cost to us? Should investors pay more for the stock of Company O than of Company N? And, if a business is worth some given multiple of earnings, was Scott Fetzer worth considerably more the day before we bought it than it was worth the following day?

If we think through these questions, we can gain some insights about what may be called “owner earnings.” These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges such as Company N’s items (1) and (4) less (c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in (c) ). However, businesses following the LIFO inventory method usually do not require additional working capital if unit volume does not change.

Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since(c) must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes - both for investors in buying stocks and for managers in buying entire businesses. We agree with Keynes’s observation: “I would rather be vaguely right than precisely wrong.”

The approach we have outlined produces “owner earnings” for Company O and Company N that are identical, which means valuations are also identical, just as common sense would tell you should be the case. This result is reached because the sum of (a) and (b) is the same in both columns O and N, and because (c) is necessarily the same in both cases.

And what do Charlie and I, as owners and managers, believe is the correct figure for the owner earnings of Scott Fetzer? Under current circumstances, we believe (c) is very close to the “old” company’s (b) number of $8.3 million and much below the “new” company’s (b) number of $19.9 million. Therefore, we believe that owner earnings are far better depicted by the reported earnings in the O column than by those in the N column. In other words, we feel owner earnings of Scott Fetzer are considerably larger than the GAAP figures that we report.

That is obviously a happy state of affairs. But calculations of this sort usually do not provide such pleasant news. Most managers probably will acknowledge that they need to spend something more than (b) on their businesses over the longer term just to hold their ground in terms of both unit volume and competitive position. When this imperative exists - that is, when ( c) exceeds (b) - GAAP earnings overstate owner earnings. Frequently this overstatement is substantial. The oil industry has in recent years provided a conspicuous example of this phenomenon. Had most major oil companies spent only (b) each year, they would have guaranteed their shrinkage in real terms.

All of this points up the absurdity of the “cash flow” numbers that are often set forth in Wall Street reports. These numbers routinely include (a) plus (b) - but do not subtract (c) . Most sales brochures of investment bankers also feature deceptive presentations of this kind. These imply that the business being offered is the commercial counterpart of the Pyramids - forever state-of-the-art, never needing to be replaced, improved or refurbished. Indeed, if all U.S. corporations were to be offered simultaneously for sale through our leading investment bankers - and if the sales brochures describing them were to be believed - governmental projections of national plant and equipment spending would have to be slashed by 90%.

“Cash Flow”, true, may serve as a shorthand of some utility in descriptions of certain real estate businesses or other enterprises that make huge initial outlays and only tiny outlays thereafter. A company whose only holding is a bridge or an extremely long-lived gas field would be an example. But “cash flow” is meaningless in such businesses as manufacturing, retailing, extractive companies, and utilities because, for them, ( c) is always significant. To be sure, businesses of this kind may in a given year be able to defer capital spending. But over a five- or ten-year period, they must make the investment - or the business decays.

Why, then, are “cash flow” numbers so popular today? In answer, we confess our cynicism: we believe these numbers are frequently used by marketers of businesses and securities in attempts to justify the unjustifiable (and thereby to sell what should be the unsalable). When (a) - that is, GAAP earnings - looks by itself inadequate to service debt of a junk bond or justify a foolish stock price, how convenient it becomes for salesmen to focus on (a) + (b). But you shouldn’t add (b) without subtracting (c) : though dentists correctly claim that if you ignore your teeth they’ll go away, the same is not true for (c) . The company or investor believing that the debt-servicing ability or the equity valuation of an enterprise can be measured by totaling (a) and (b) while ignoring (c) is headed for certain trouble.

To sum up: in the case of both Scott Fetzer and our other businesses, we feel that (b) on an historical-cost basis - i.e., with both amortization of intangibles and other purchase-price adjustments excluded - is quite close in amount to (c) . (The two items are not identical, of course. For example, at See’s we annually make capitalized expenditures that exceed depreciation by $500,000 to $1 million, simply to hold our ground competitively.) Our conviction about this point is the reason we show our amortization and other purchase-price adjustment items separately in the table on page 8 and is also our reason for viewing the earnings of the individual businesses as reported there as much more closely approximating owner earnings than the GAAP figures.

Questioning GAAP figures may seem impious to some. After all, what are we paying the accountants for if it is not to deliver us the “truth” about our business. But the accountants’ job is to record, not to evaluate. The evaluation job falls to investors and managers.

Accounting numbers, of course, are the language of business and as such are of enormous help to anyone evaluating the worth of a business and tracking its progress. Charlie and I would be lost without these numbers: they invariably are the starting point for us in evaluating our own businesses and those of others. Managers and owners need to remember, however, that accounting is but an aid to business thinking, never a substitute for it.

Conclusion

Buffett has been very consistent over the years with his answer on what he defines intrinsic value. Here are the key things we learnt about from Warren on what is intrinsic value, and how to estimate it:

Intrinsic value is the present value of all the future cash flows that a business can generate for its owners, discounted at an appropriate interest rate.

To estimate future cash flows, start with current owner earnings, not GAAP reported. The formula is:

Reported earnings plus

Depreciation, depletion, amortization, and other non-cash charges

lessThe average annual amount of capitalized expenditures required to fully maintain the business’s long-term competitive position and unit volume plus any additional working capital to maintain its competitive position and unit volume, included in maintenance CAPEX.

Unlike a bond, where cash flows are explicit, a stock’s future cash flows are not printed on the certificate. They must be estimated by the security analyst, which is us, the investors.

You must discount these estimated future cash flows back to today using an appropriate discount rate. This discount rate isn’t calculated by using CAPM, WACC, or any academic formula. He uses the long term US bond yield, but does sometimes adjust for uncertainty. The adjustment is usually unnecessary, as he then applies a margin of safety. He will not pay for that estimated intrinsic value, he pays below it.

The discount rate accounts for the time value of money and risk.

Focus on what the business produces, not the market price. Intrinsic value is independent of stock market fluctuations or analysts’ opinions.

Buffett only attempts to calculate intrinsic value for businesses he understands reasonably well. He avoids many early tech or unpredictable businesses because the future cash flows are too uncertain, so it’s very difficult to make an educated guess on intrinsic value. Even if the business is uncertain, with low amounts of capital and a big margin of safety, he would still buy. However, this type of uncertainty only applies to cyclical type businesses that have proven products. Uncertainty isn’t necessarily bad and depresses market price, which created bigger discrepancies between intrinsic value and price. If uncertainty is related to unproven products, very unstable cash flows, or significant risks that don’t protect downside, then he wouldn’t invest as he cant make an educated and conservative guess on the future (even if near term) of the company.

Buffett considers the cash flows over the entire life of the business, potentially decades or even hundreds of years into the future. This is very difficult to estimate, so you can make a reasonable guess on the next few years of cash flows and then assume no growth in perpetuity, making the terminal value the same as:

Owner Earnings / Appropriate Interest Rate (usually a 10-30 year bond yield)

Always remember it’s far better to be approximately right than precisely wrong. So don’t stress about calculating every decimal, if the margin of safety is big enough, it will be clear its undervalued. Always start assuming no future growth. If the company offer a satisfactory margin of safety assuming no growth when its more likely for it to grow, the margin between intrinsic value and current price is much bigger and undervaluation is highly probable.

I hope I helped you to understand what intrinsic value actually is, how to actually calculate it, how to calculate owner earnings, and how you can apply it in your decision making when investing!

This post has been created for educational purposes only. It is not advice or recommendation for investing in securities. Security investing always carries risk.

Excellent synthesis of the “Bird in the Hand” philosophy. This post highlights a crucial distinction many miss: intrinsic value isn't a static accounting figure, but a dynamic estimate of future cash flows. The comparison between a stock certificate and a bond with “unprinted coupons” is one of the most effective ways to understand why business predictability is more important than market volatility.

Buffett mentions using the long-term government bond rate as the discount factor, yet Charlie Munger often emphasizes “opportunity cost” as the ultimate filter. In a low-interest-rate environment, do you believe relying on the risk-free rate risks overestimating intrinsic value, or should an investor's personal “hurdle rate” always take precedence?

Warren Buffett: If we could see, in looking at any business, what its future cash inflows or outflows from the business to the owners would be over the next hundred years, or until the business is extinct, and then discount that back at the appropriate interest rate, that would give us a number for intrinsic value.

.

The exact Intrinsic Value formula of the above mentioned definition by Buffett is :

EARNING POWER VALUE

= Earning ÷ Discount Ratio

The Earning could be Operating Profit, Net Profit, OCF or FCF.

FASB research has concluded that Operating Profit is better than the cash flow in deriving the actual long term future cash flow.

I would suggest to choose the lowest among Operating Profit, Net Profit, OCF and FCF.