Portfolio Allocation, May 2026

Author Notes:

The portfolio’s return since inception on April 2026 is roughly 3%, vs the S&P 500’s 7.7%.

The general stock market keeps on booming, and I don’t believe this type of performance is sustainable.

I make no attempt to predict where the market is going. However, I do believe speculation at levels like this will lead to the eventual reversion of price. If this occurs, prices, even of undervalued securities, will be temporarily affected.

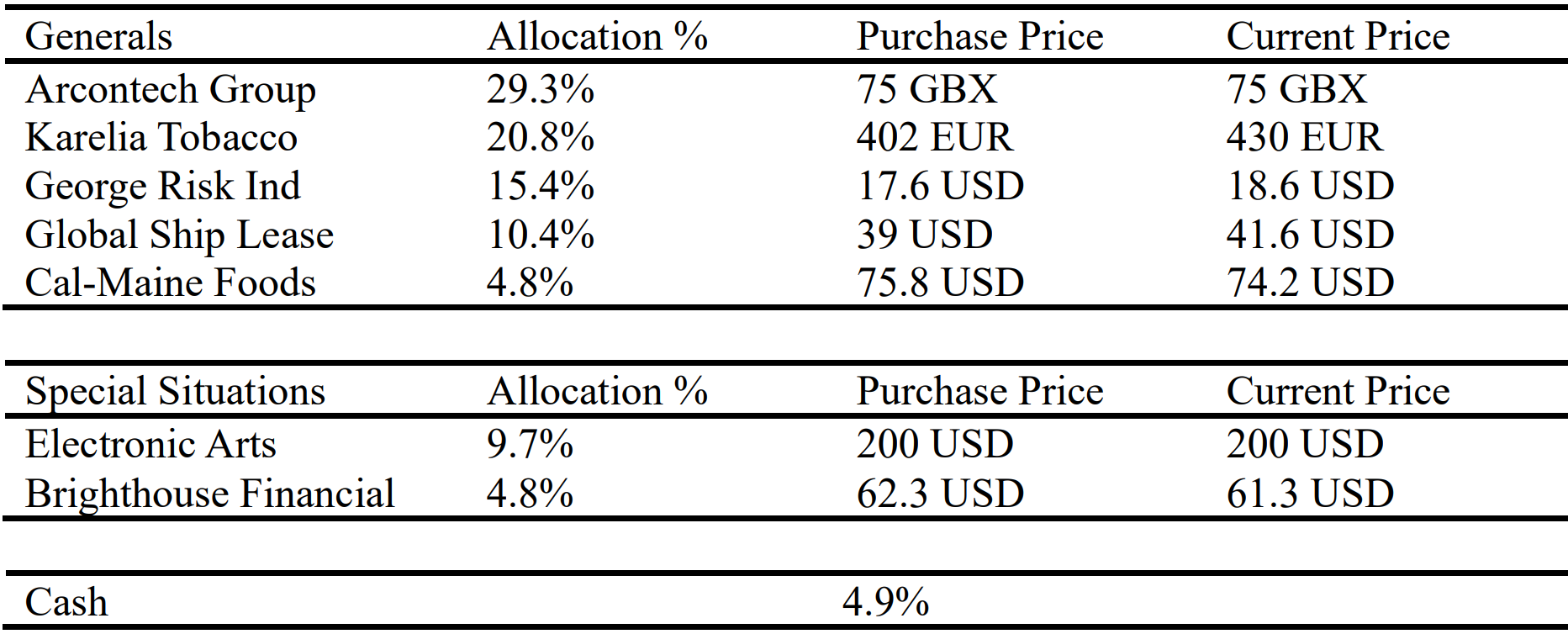

Holdings as of May 2026:

Farmer Brothers has been successfully acquired by Royal Cup Coffee & Tea, in the expected timeframe. The deal was an all-cash transaction at $1.29 per share, and with a purchase price of $1.26, the position has returned 2.4% in just one month - equivalent to an annualized return of nearly 30%. I find the return of said investment highly satisfactory, and while I’ll continue to look for these types of special situations, I do not expect future investments to yield this annualized amount.

A new security has been added to the portfolio, Electronic Arts. The offer is $210/share in cash. Shareholder approval has been secured; however, the transaction requires extensive global regulatory reviews, including a CFIUS clearance. The probability of the deal closing within the expected timeframe, which is around mid-2026, is currently high, following reports that the final batch of international regulatory clearances was secured in early April 2026. If the deal successfully closes, we could expect an annualized return of more than 25%.

The Centessa Pharmaceutical position has been sold completely. This is due to the timeframe of the CVR payout. While the acquisition is still a high probability event, the CVR could be realistically paid in around 5 years. After evaluating the opportunity cost, this investment is not for me. The sale of Centessa has been kept in a cash sleeve for future allocation into new securities.

I have also cut the Brighthouse Financial position by half, due to state insurance regulators in the US being under pressure to be stricter with private equity firms (such as Aquarian) that buy life insurers. Both the excess gain from the successful Farmer Brothers acquisition and the cash from the sold shares in Brighthouse have been deployed into Arcontech, making it the biggest holding by far.

*General Situations & Co. is not a real or existing partnership, nor does it manage outside capital of any kind. It is simply a Substack newsletter. This is not financial advice.